Since 2020 the increasing number and severity of natural disasters such as wildfires and hurricanes have cast home insurance markets into turmoil, leading to an explosive rise in premiums across the country.

Unaffordable premiums now represent one of the most tangible ways that climate change is affecting everyday Americans. And this election season, insurance commissioners – the state officials in charge of overseeing these markets – are suddenly in the hot seat.

Insurance commissioners have historically operated outside of the spotlight, steeped in financial statements and wonky regulations.

In the 11 states (including Oklahoma) that elect their commissioners – the rest appoint them – these races have rarely received much interest. In some elections, incumbents don’t even face a challenger. In others, state data show that as many as 17% of voters simply skip over that section of their ballots.

“It’s just not something [voters] pay attention to until things go wrong,” said Dave Jones, who served as California’s insurance commissioner from 2011 to 2019. “Right now, things are going wrong.”

In recent years, insurance companies have found themselves increasingly on the hook for homes hit by wildfires and severe storms.

In Louisiana, a parade of back-to-back hurricanes and extreme storms in 2020 and 2021 caused insurers to pay out well over twice as much money as they brought in. Similarly, in Colorado, where the state has experienced more than 40 billion- dollar disasters in the past decade, insurers lost money in eight of the past 11 years.

State Farm – the largest writer of insurance in Oklahoma “with about 28% of the market share” – lost $13 billion nationwide last year, Oklahoma Insurance Commissioner Glen Mulready told Southwest Ledger.

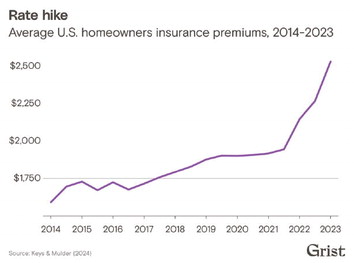

To pay for all this damage, premiums have been skyrocketing nationwide. According to a 2024 study of insurance rates, the average home premium rose 33% between 2020 and 2023. In disaster-prone areas like Florida, the Gulf Coast and California, rates have increased even more, with some insurers pulling out of markets entirely.

Mulready related earlier this year that when he appeared on a panel of insurance commissioners across the country, South Carolina’s lamented that coastal apartments in that state can’t get insurance because of the extensive damage from hurricanes in recent years.

According to Brad Berrong of Weatherford, a second-generation insurance agent, more than 40,000 homes in the U.S. were destroyed by wildfires in 2022.

An insurance carrier notified one of its customers in rural Custer County earlier this year that their property insurance policy would not be renewed “because of the perceived exposure of the home to wildfire,” Berrong said.

“Four years ago this wasn’t even a conversation topic” in Oklahoma, he said.

Starting in 2015, California was hit with billion-dollar wildfires every year until 2023.

Insurance companies are ‘pulling back’ because of losses Most insurance companies “are pulling back because they’re losing money and can’t make it up in volume,” Berrong said.

If an insurance agency has a loss ratio of more than 65% – if it pays out on claims more than 65 cents of every dollar it collects – “it’s losing money,” said Chris Mosley, a Chickasha insurance agent for 31 years.

Insurers “are not nonprofits,” Mulready quipped.

Many property owners and insurance agents “are having to scramble,” Berrong said. “We’re having to shop about 70% of our business.”

Insurance carriers “have to protect their assets to remain profitable,” he said. “Unfortunately, we don’t have the methodology to charge you an appropriate premium” for coverage against wildfires and hail damage “in order to preserve the capital” of insurance companies.

“These are unprecedented times,” Mosley told the Ledger in January. “I haven’t seen it this way before.”

Inclement weather is taking a heavy toll on property owners and insurers alike.

Commissioner Mulready has firsthand experience about roof replacement costs. A year and a half ago he received an estimate on replacing the roof of his 4,000 square-foot house in Tulsa: $20,000. Eighteen months later, though, the estimate had risen by 30%, to $26,000.

Roof repairs have gotten so expensive that insurance companies are “bifurcating” their property insurance coverage, Weatherford insurance agent Berrong told the Ledger.

“There’s one deductible category for events such as fire, lightning, theft, frozen water lines and pipes, falling objects, or a car plowing into the side of your house,” Berrong said. For a typical peril of that nature the deductible may be 1% of the value of the structure, he said. But coverage for wind and hail damage, and in some cases wildfire, may be twice as expensive: 2% of the value of the structure.

For example, for a house valued at, say, $200,000, the out-ofpocket deductible for wind or hail damage would be $4,000 per occurrence.

“We have seen deductibles on commercial buildings as high as 5% of the value of the structure,” former mayor Mosley told the Ledger.

“This means you are taking more risk on wind and hail, but the insurer can try to keep your premiums from going absolutely crazy” by raising the deductible, Berrong said.

Mosley concurred. “Why spend more money annually for a higher insurance premium when you can lower that cost by choosing a higher deductible that you can expect to pay only rarely?”

Deductibles for roof repair/replacement much higher now What used to be a simple, affordable deductible for roof repair/ replacement – perhaps $1,000 or $2,500 – has soared in Oklahoma.

Repairing or replacing a damaged roof today “costs three times as much as it did just four years ago,” Berrong said. “The No. 1 thing insurance pays for on homes is roofs – but the cost has become so expensive.” Of all the residential damage claims in Oklahoma, “hail is No. 1 and wind is No. 2,” he said.

“We are a ‘weather state’ in that we have our share of wind and hail,” Mulready noted.

Almost two-thirds of all property insurance claims in Oklahoma are hail-related, and 92% of those claims are for damage from hailstones 2 inches or smaller in size, Mosley said.

A composition shingle Class 4 roof should be capable of withstanding hail up to 1 inch in diameter and be warrantied by the manufacturer to survive winds of 65 miles per hour.

If you’re installing a metal roof, “look at the tensile strength of the material,” Berrong recommended. “The tensile strength makes it tougher to dent.” Cosmetic damage is not covered by insurance, he added.

On a commercial roof, install high-quality TPO (thermoplastic polyolefin) waterproofing membrane to avoid leaks.

Ensure that a home’s attic is properly ventilated; otherwise, summertime heat will cause blistering of the shingles. “You want that roof to breathe,” Mosley said.

In addition to requiring higher deductibles, many insurers no longer offer replacement cost on roofs, especially if it is 10 years old or older. Instead, coverage is depreciated based on the age of the roof. “Consequently, your insurer may cover only half of the cost of a roof replacement,” Berrong said. Insurance commissioners are in the voters’ spotlight Rising insurance costs are prompting voters to take a closer look at elected commissioners who regulate the industry in their home states – and it is forcing candidates to more thoroughly consider insurance shifts and climate change in their platforms.

States have been regulating their insurance markets for more than 150 years; New Hampshire appointed the nation’s first commissioner in 1851.

These regulators are tasked with setting reasonable limits on how much insurance companies can charge for home, car, health, and life insurance. They also oversee how insurers manage their money, so they have enough to pay their bills when disaster strikes. For the vast majority of their history, insurance commissioners haven’t thought much about climate change.

“When I came in, climate change was kind of a footnote,” said Mike Kreidler, Washington’s outgoing insurance commissioner, who was first elected to the office in 2000. “That was something that bothered me a lot, because I saw the risks.”

Kreidler’s early attempts at climate action were met with fierce resistance. As an early member of the National Association of Insurance Commissioners’ climate working group, he recalled some of his peers asking him to remove the word “climate change” from his proposals. “I took a lot of abuse back then on these issues,” Kreidler said. “It’s not something that a number of commissioners wanted to talk about.”

Climate change has “become a number one issue for insurance regulators across the United States,” former California Insurance Commissioner Jones said.

It has become an important issue for voters as well. Over the last few years, major insurance companies have started backing out of high-risk parts of the country. California’s largest insurer, State Farm, stopped accepting new customers, and will not renew policies for roughly 30,000 homeowners and renters living in certain risky parts of the state.

In Florida, so many homeowners have been denied coverage that the government-created “last-resort” program is now the largest insurance provider in the state. This trend – of fewer and more expensive options – is leading some frustrated voters to turn their attention toward their elected leaders.

This year, North Carolina has become the battleground of one of the nation’s first insurance commissioner races centered largely around climate impacts. Coastal storms and hurricanes are taking a worsening toll on the state.

Hurricane Helene left widespread devastation late last month in North Carolina, especially in the Asheville area. And Hurricane Florence caused more than $16 billion in property damage in 2018.

Americans moving to disaster-prone areas Ben Keys, an economist and professor of real estate and finance at the University of Pennsylvania’s Wharton School, says that this trend does not explain the recent hike in insurance costs. He and a colleague recently analyzed premiums from 47 million homeowners across the country.

Over the past 40 years, Americans have been moving to more disaster- prone regions of the U.S. South and West. “A hurricane cutting the Gulf side of Florida now encounters more houses, more businesses, more roads, more infrastructure than it did 40 years ago,” Keys said.

At the same time, climate change has been increasing the frequency and severity of extreme storms and wildfires in those fast-growing regions. Finally, when disaster strikes, inflation and labor shortages have driven up the cost of rebuilding.