American credit card debt neared a trillion dollars by the end of last year.

Lending Tree reported that the mountain of credit card debt climbed to $925 billion. TransUnion said credit card debt totaled $930.6 billion in the fourth quarter of 2022, an 18.5% increase from a year earlier.

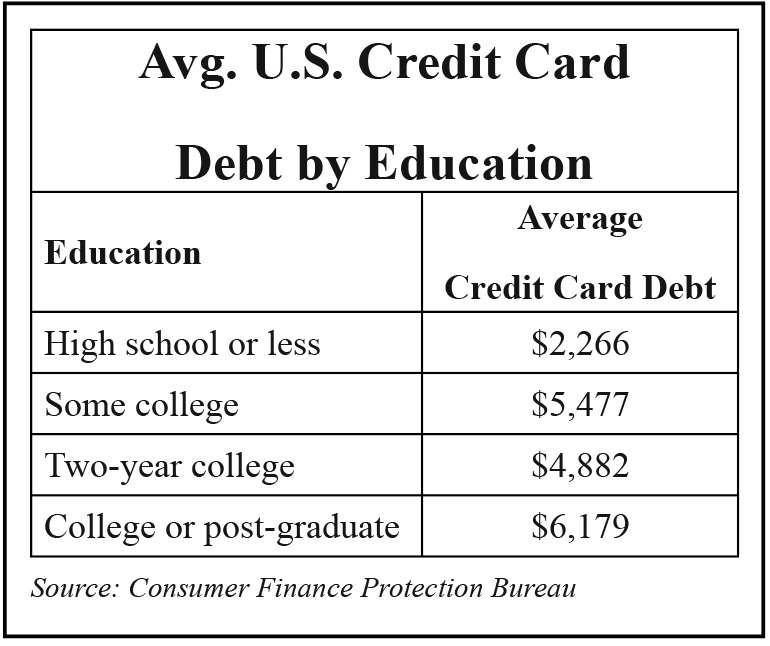

Carrying thousands of dollars in credit card debt has become normal for many Americans.

The average credit card balance is $5,589, according to a 2022 Experian report. TransUnion reported the average balance rose to $5,805 by the end of last year.

According to Lending Tree, New Jersey had the highest average credit card debt last year, at $7,872; in Oklahoma, the average was $6,207; in Texas, $6,999. The national average was $6,569, Lending Tree reported.

On the heels of another interest rate increase by the Federal Reserve, which is pushing prices up, credit card annual percentage rates are nearing 20%, on average, according to Bankrate.

This is occurring at the same time that more consumers are relying on credit to finance necessities such as groceries and rent.

At nearly 20%, making minimum payments toward an average credit card balance would take more than 17 years to pay off the debt and cost more than $8,213 in interest, Bankrate calculated.

“Whether it’s shopping for a new car or buying eggs in the grocery store, consumers continue to be impacted in ways big and small by both high inflation and the interest rate hikes implemented by the Federal Reserve,” said Michele Raneri, vice president of U.S. research and consulting at TransUnion.

Overall, an additional 202 million new credit accounts were opened in the fourth quarter of 2022, led by originations among Generation Z, or adults ages 18 to 25, and the number of credit cards in circulation in the U.S. hit a record 518.4 million. The Census Bureau pegged the United State population at 334 million on Jan. 1, 2023.

As the number of credit card accounts rises, more new customers are subprime borrowers, generally meaning those with a credit score of 600 or below, according to TransUnion, in part because of the flood of younger borrowers gaining access to credit cards.

Simultaneously, delinquencies rose as lenders expanded access to less experienced credit users, the report found. TransUnion defines a delinquency as a payment that’s 60 days or more overdue.

Every dollar of credit card debt a consumer pays down has an average guaranteed, tax-free return of about 20%, said Ted Rossman, senior industry analyst at Bankrate.

In a related matter, nearly two of every three Americans were living paycheck to paycheck in December, up from 61% a year earlier, LendingClub reported.