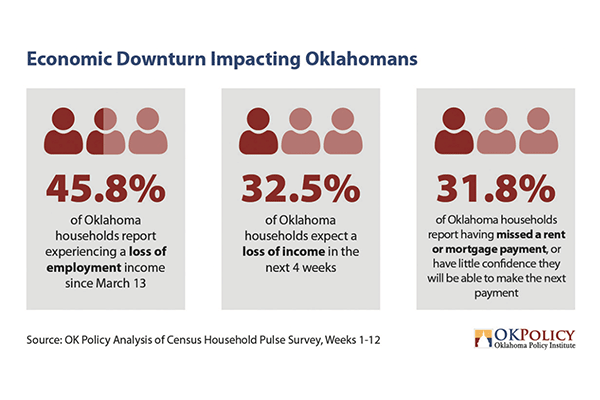

Many Oklahomans are in a financial crunch. The pandemic has taken an economic toll on households across that state, which we see clearly in the most recent Census Household Pulse Survey.

The survey at right shows that many of our friends and neighbors have lost jobs and/or income during the pandemic. More than three in 10 households say they have missed a mortgage or rent payment or are unsure they can make their next payment. These families are experiencing real financial distress, and some may look to quick consumer loans to help bridge the gap.

Changes that went effect last month in Oklahoma will offer higher dollar loans but at a significant long-term cost. Starting

Aug. 1, 2020, payday loans (short-term loans of $500 or less) can no longer be issued.

Instead, these lenders can now offer longer-term loans in higher dollar amounts: up to $1,500 with terms of up to 12 months. Oklahoma consumers should be aware of the potential dangers of these new installment loans. Just like the payday loans they replace, they are designed to trap borrowers in long-term debt.

INSTALLMENT LOANS COMMAND HIGH INTEREST RATES

Consumer lenders can now offer installment loans of up to $1,500 to Oklahoma borrowers. These loans are paid back in equal monthly payments and carry a very high interest rate.

The law that created these loans in Oklahoma – Senate Bill 720, which Governor Kevin Stitt signed on April 18, 2019 – allows lenders to charge 17% interest each month, which amounts to an annual percentage rate of 204%.

All small loans executed under the Oklahoma Small Lenders Act must be unsecured, have a loan period between 60 days and 12 months, be fully amortized and payable in substantially equal periodic payments, and contain no prepayment penalty.

The primary reason these loans are problematic is that those equal payments disguise the amount of interest that borrowers are really paying.

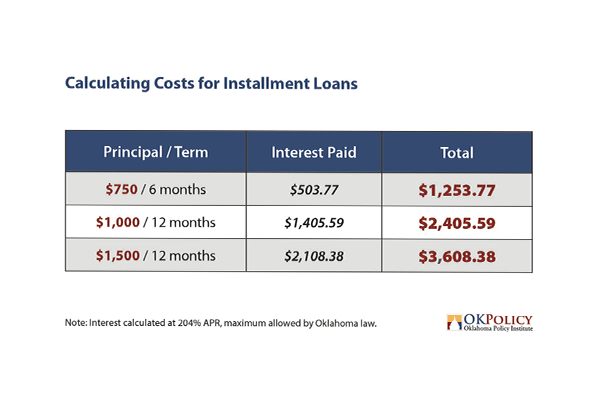

A borrower who takes out a $750 installment loan for a term of six months will pay $503.77 in interest. A $1,000 loan paid back over 12 months will carry $1,405.59 interest. The maximum loan amount of $1,500 will cost $2,108.38 in interest for a 12-month loan.

With such a high interest rate, installment loan borrowers can easily end up paying more in interest than they actually borrowed, and this creates further financial hardship. (See table.)

THESE LOANS UNAFFORDABLE FOR MANY

In phasing out the availability of payday loans and replacing them with installment loans, policymakers were attempting to offer more affordable short-term loans with better terms to borrowers. Unfortunately, there are not many protections for borrowers with these new installment loans.

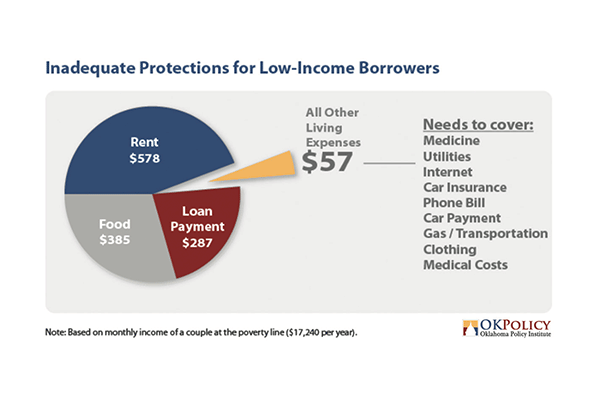

Lenders must make sure that monthly payments do not exceed 20% of the borrower’s gross income (before taxes and deductions). A couple with income at the poverty line ($17,240 per year) could be approved for a payment of up to $287 per month that would have to come out of their $1,297 each month in take-home pay. (See pie chart at bottom right.)

That leaves just over $1,000 for rent, utilities, food, transportation, and other basic needs, and it will not be enough. For example, fair market rent for a one-bedroom apartment in Oklahoma is $578, and the U.S. Department of Agriculture estimates that a couple needs at least $385 per month for food. After housing, food and loan costs are taken out of their monthly income, borrowers would be left with just $57 to pay for utilities, transportation, medical costs, or any other everyday expense.

If a borrower cannot pay back the loan, he/she can be declared in default as soon as one day after their first missed payment. The authorizing legislation also allows lenders to request that the borrower’s wages be garnished for repayment, making it even more difficult to meet basic needs.

INSTALLMENT LOANS ARE DANGEROUS

Middle to high- income Oklahomans are likely to have access to more affordable sources of credit, such as bank loans and credit cards, should they experience temporary financial setbacks. Low income Oklahomans are less likely to have an established credit history, making these more affordable options unavailable to them.

So those who are least likely to be able to afford these high-interest loans will be target customers for installment lenders. This has the potential for economic disaster.

Oklahoma received $1.2 billion from the federal CARES (Coronavirus Aid, Relief, and Economic Security) Act to spend on coronavirus relief, and more of that funding needs to go directly to families impacted by the pandemic so they don’t have to rely on potentially harmful short-term, high-interest loans.

Courtney Cullison, a native Oklahoman, is a policy analyst focusing on issues of economic opportunity and financial security. Before joining OK Policy, she worked in higher education, holding faculty positions at the University of Texas at Tyler and at Connors State College in eastern Oklahoma. She received an Honors B.A. in political science from Oklahoma State University, and an M.A. and Ph.D. with emphasis in congressional politics and public policy from the University of Oklahoma.