Deposit Market Shares

OKLAHOMA CITY – The number of banks in the Sooner State held steady throughout the second and third quarters of 2019, but is one less than the FDIC counted in the first quarter of last year and seven fewer than operated in Oklahoma two years ago.

Oklahoma had 201 banks at the end of both the second and third quarters of 2019, according to the Federal Deposit Insurance Corp. In comparison, the FDIC counted 208 banks operating in Oklahoma in 2017.

Nevertheless, the assets of the surviving institutions grew 18.3% during that period: from $114.89 billion in 2017 to $135.97 billion in the third quarter of 2019 (July, August, and September).

Of the 201 banks:

• 73 of them (36.3%, an increase of one bank from the second quarter) had assets of less than $100 million;

• 54 of them (or 26.9% of the banks, an increase of two from the second quarter) had assets of $100 million to $250 million;

• 62 of them (30.8%, three fewer than in the second quarter) had assets ranging from $250 million to $1 billion;

• 10 banks (5%) reported assets of $1 billion to $10 billion; and

• Two banks have assets valued at greater than $10 billion each.

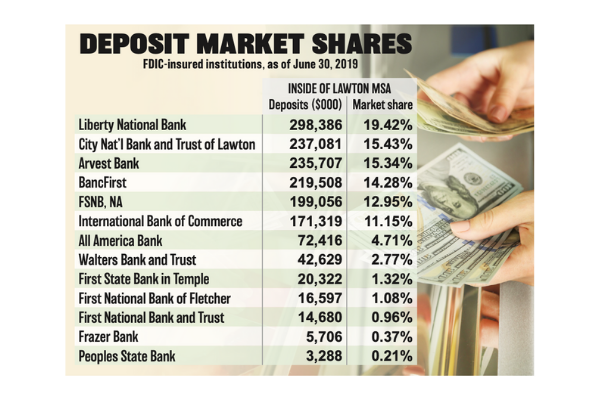

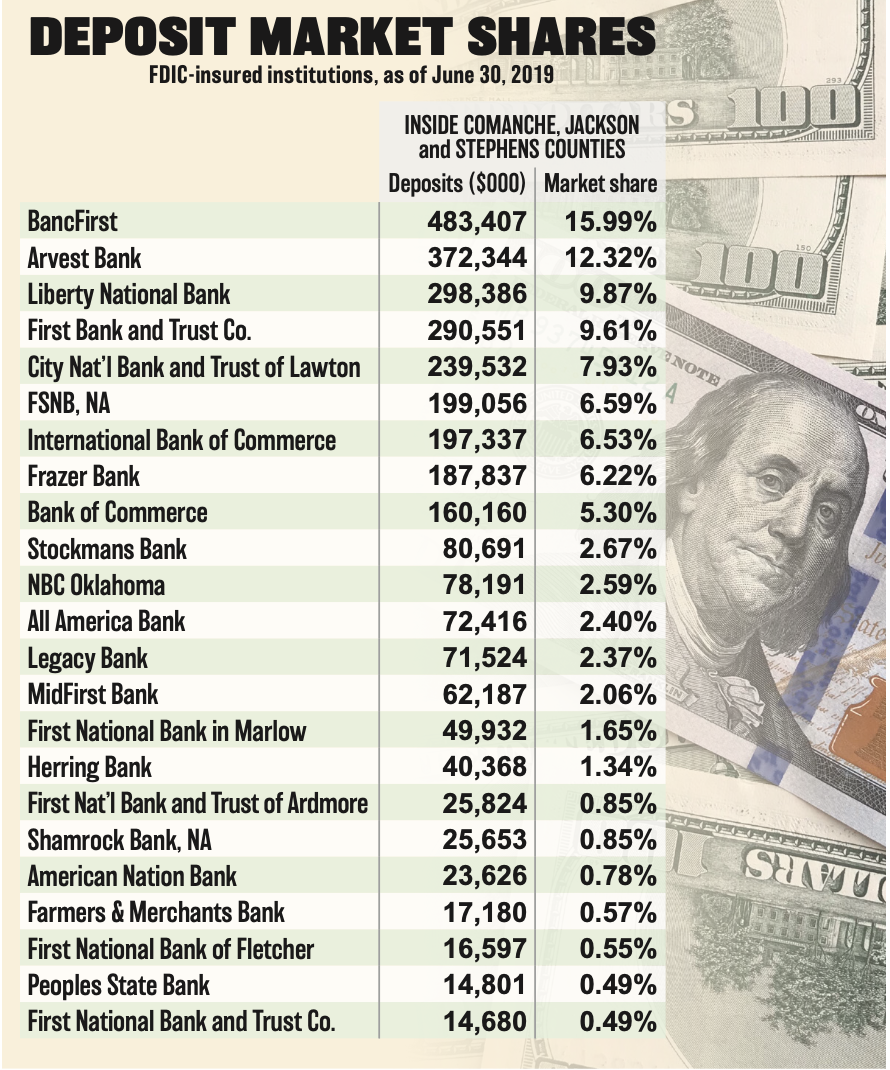

The current state profile shows that for the third consecutive quarter, Lawton had 13 banks with $1.5 billion in deposits; Oklahoma City, 72 banks with deposits of $33.9 billion (an increase of one bank and $3 billion in assets); Tulsa, 57 banks with $26.6 billion in deposits (two fewer banks but $1.2 billion more in assets); Fort Smith-Arkansas/ Oklahoma, 20 banks holding

$4.5 billion in deposits (one less bank and $160 million less in assets); and Enid, 14 banks with $1.5 billion in total deposits.

The banks in those five markets constituted 176 of the 201 banks in the state.

In an examination of the quality of assets held by Oklahoma banks, the FDIC found that past-due and non-accrual loans have constituted 1.6% of total loans over the last 11 quarters. Net loan losses have grown from 0.03% in the first quarter of 2019 to 0.06% in the third quarter; still, that’s lower than the 0.11% rate of 2017 and the 0.09% rate in 2018.

Growth in non-farm employment in Oklahoma during the third quarter of 2019 slowed to 0.4%, half of the 0.8% growth rate of the second quarter and significantly less than the 1.5% growth rate in 2018, the FDIC reported. During the third quarter of this year, employment:

• slipped another 1.5% in manufacturing, which constituted 8% of the total state labor force; employment in the manufacturing sector decreased by 1.5% during the second quarter of 2019, too.

• grew 2% in non-manufacturing goods producing, which also accounted for 8% of the workforce; this sector realized 4% growth in the second quarter of this year and 6% growth in the first quarter.

• increased seven-tenths of a percent in the private service-providing sector, compared to 1% in the second quarter of 2019. This sector comprised 63% of the Oklahoma workforce.

• declined in the government sector for the third consecutive quarter of 2019. This sector, which accounted for 20% of the labor force, shrunk 0.3% in the third quarter, 0.1% in the second quarter, and 0.3% in the first quarter. Employment in Oklahoma’s public sector also fell 0.4% in 2018 and 0.9% in 2017, the FDIC reported.

The overall unemployment rate in Oklahoma, seasonally adjusted, was 3.2% in the second and third quarters of 2019 and 3.3% in the first quarter. Late last month the U.S. Bureau of Labor Statistics reported that unemployment in Oklahoma inched up to 3.4% in November, compared to the national unemployment rate of 3.5%. The state’s jobless rate was 3.4% in 2018 and 4.2% in 2017, FDIC ledgers reflect.

Non-business bankruptcy filings per 1,000 Oklahoma residents was 2.38 during the third quarter of 2019, a decline from the 2.6 rate of the second quarter, the FDIC report showed.