TransUnion is tracking four key trends of COVID-19’s impact on the insurance industry as we move into 2021 and beyond. The pandemic has become a defining event to accelerate the industry’s transition to becoming more digital and better understand clients’ needs.

In a survey of 3,148 U.S. consumers with active automotive, homeowners, renters and/or life insurance policies in early December, TransUnion polled four trends highly impacting the key generations in today’s economy: Baby Boomers, Gen X, Millennials, and Gen Z. The main takeaway is the expectation that impacts of the pandemic will be felt well into next year.

“COVID-19 pushed the need for nascent, innovative digital solutions and services to the forefront of standard insurance industry operation. The unpredictable environment that lies ahead indicates consumers and businesses will increasingly rely on and choose insurers offering online resources and tools that can best meet their needs, particularly as digital adoption continues to grow,” said Mark McElroy, executive vice president and head of TransUnion’s insurance business. “The 2021 trends and insights revealed by our latest consumer survey can help insurers develop a better understanding of consumers and businesses while also equipping them with in-formation to build a reliable basis for trust with those they serve.”

The financial and economic challenges brought forth by COVID-19 will continue to impact consumers and businesses, potentially leading to profitability impacts for insurance carriers next year and beyond. The survey indicated respondents are primarily concerned about being able to pay for their auto insurance bill (44%), followed by their car payment (26%), mortgage payment (23%) and life insurance bill (22%).

Many insurance carriers, in an effort to provide financial relief to consumers, have and will continue to return money back to customers, up to an estimated $14 billion. This doesn’t quell the concern of consumers regarding their ability to cover their premiums on time.

Fewer short-term claims in the commercial automotive space are expected, with insurers facing short-term stability in underwriting performance. The factors contributing to this trend are less congested roads and less overall miles driven. For insurers to remain competitive as the pandemic wanes, strengthening engagement with customers will be tantamount.

Consumer needs, behaviors, and preferences are shifting, and insurers must have a greater understanding of those individualized needs to remain competitive. Remote work and ongoing financial hardship have produced a significant reduction in miles driven which has led to fewer claims.

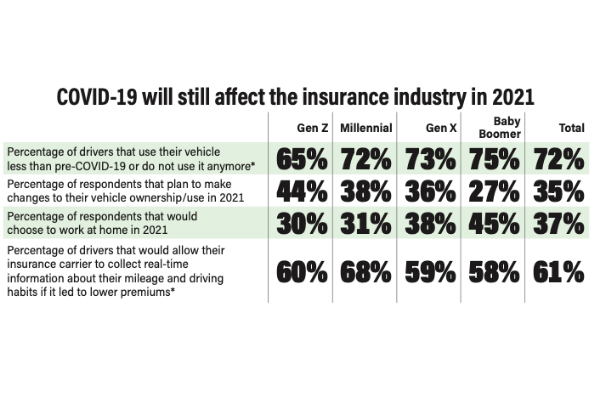

For respondents who own or lease a car (90%), TransUnion’s survey indicated that 72% used their vehicle less in the time since COVID-19 was named a global pandemic or don’t use their vehicle anymore. A full 35% of respondents plan to make changes to their vehicle ownership and/ or use in 2021, with Gen Z leading the pack at 44%.

In addition, the survey found 61% of drivers would allow their insurance carrier to collect real-time information about their mileage and driving habits if it could lower their premium. Look for insurers to push usage-based insurance and telematics programs even more in the coming months to take ad- vantage of consumer wants and needs.

Respondents also are strongly preferring work-at-home and remote programs —at a tune of 37%—with 31% preferring a hybrid between the two. Baby boomers topped the list, with 45% of respondents claiming they would choose to work at home in 2021, if they were given the option.

The remote revolution was already gearing up, but the pandemic accelerated the trend by years or even decades. As such, a decline for commercial real estate de- mand might follow as businesses pivot to a new normal and find cost-saving measures a positive effect of COVID-19 for the long-term. This would produce a decline in needs for commercial insurance on office space, requiring insurers to address a loss in revenues.

While the industry as a whole has been embracing technology and digitization, the pandemic strengthened that resolve and efforts will continue well into the next decade. Competitiveness in the marketplace had already pushed the industry forward, with digital adoption growing by 20% globally in the past year. Consumers expect ease of use through their smartphones, tablets and computers in choosing their insurer, submitting claims and accessing their policy information.

COVID-19 social-distancing guidelines and stay-at-home mandates also have exacerbated the need for digitally-driven solutions within the life insurance industry. One such way life insurers are meeting this need is with accelerated underwriting, which leverages third-party data to streamline the traditional underwriting process (which can require an in-person visit to an applicant’s home).

Extreme weather events will drive an increase in the number and severity of disaster-related claims in 2021 and beyond. While the global impact of COVID-19 stole most of the headlines, the U.S. experienced record-breaking numbers of natural catastrophes over the past year.

A full 21% of respondents said they were impacted by natural disasters in the last 12 months. Recent weather trends, signs of climate change, and ever growing exposure in high-risk areas suggests the industry will likely continue to see this demonstrable increase in the frequency and severity of natural disaster-related claims.

While loss mitigation opportunities improve, insurers will need to continuously assess risk and implement proactive strategies to address operational challenges and manage risk for businesses and consumers.