Ranchland values in the Tenth Federal Reserve District, a multistate region which includes Oklahoma, grew notably in the first quarter of 2026. According to survey respondents, ranchland values increased rapidly from a year ago and jumped to new record highs alongside ongoing strength in the cattle sector.

Despite persistent weakness in the crop sector, cropland values increased modestly for the first time since early 2024. Farm loan interest rates dropped slightly closer to longer term average, and lenders reported that government payments provided support to farm finances. Credit conditions continued to show signs of gradual deterioration as measures of repayment rates, carryover debt, and loan restructuring remained similar to a year ago.

The outlook for major industries in the U.S. farm economy remained starkly split as profit opportunities for crops were narrow and high cattle prices continued to benefit many operations in the sector. Uncertainty and concerns about fertilizer and fuel costs have lingered through early May and were likely considered by respondents during the survey period at the end of March. While higher prices for key inputs may increase costs for producers, the accompanying increase in crop prices has likely offset additional margin compression.

Despite ongoing challenges for crop producers, strong cattle revenues, government payments and strong farmland valuations are likely to continue providing support to the sector and help limit financial stress.

Ranchland values in the Tenth District rose sharply in early 2026 and cropland values increased modestly. The average value of ranchland in the region increased by nearly 11% from a year ago during the first quarter and reached new record highs. After stabilizing over the past year, the value of non-irrigated and irrigated cropland increased by about 2.5% and 4%, respectively, and remained near historic highs.

Cash rents for ranchland increased steadily, but cropland rents showed further signs of softening. The average cash rent on ranchland in the region increased by about 2% over the past year and, similar to land valuations, reached a new record high. Despite slightly higher cropland valuations, rents on that land declined by about 1.5%.

The recent decline in farm loan interest may have provided some support to farmland markets. The average rate on all types of agricultural loans declined slightly from the previous quarter and moved nearer to recent historical averages. The average rate on farm real estate loans was about 100 basis points lower than the beginning of 2025 and was only about 40 basis points above the 25-year average.

Payments from the Farmer Bridge Assistance (FBA) program have also provided support to farm finances in recent months. About 80% of respondents in the 10th District expected payments from the program to provide at least modest support to farm income and credit conditions. Expectations about the impact of the FBA program were similar to the outlook for distribution of American Relief Act payments in 2025.

Alongside strength in the cattle sector and support from government payments, deterioration in farm finances slowed slightly. The pace of decline in farm income and borrower liquidity dropped slightly in the first quarter. The share of lenders reporting that farm income was lower than the same time a year ago increased in the Mountain States and Nebraska but declined in other states; respondents in Oklahoma reported improved incomes.

The pullback in capital spending also eased slightly while household spending grew gradually. The pace of decline in farm borrower capital spending was slightly slower than the previous quarter and the rate of change in household spending was steady. The share of lenders reporting that household spending was higher than the same time a year ago has remained near 40% since late 2023 and continued to signal gradual upward pressure on living expenses.

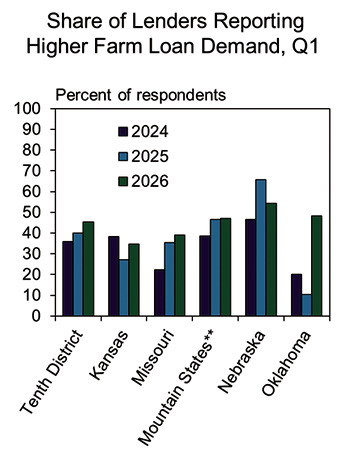

With elevated production costs and more restrained liquidity, loan demand increased steadily. The pace of increase in non-real estate loan demand was similar to recent quarters and was expected to stay steady in the coming months. The share of lenders reporting that loan demand was higher than the same time a year ago was relatively unchanged in most states but increased notably in Oklahoma.

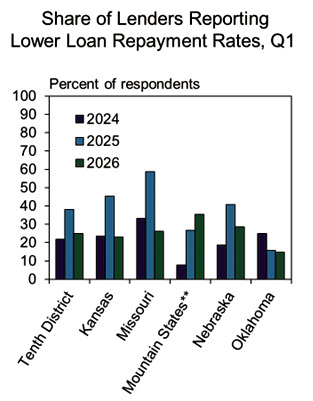

Deterioration in loan repayment was modest, but persistent. The pace of decline in farm loan repayment rates picked up slightly from the previous quarter but was less pronounced than in early 2025. The share of lenders reporting that loan repayment rates were lower than the same time a year ago dropped to around 20% in almost all states except the Mountain States.

Instances of unpaid carryover debt remained slightly elevated as crop producers renewed operating loans after a third year of limited profit opportunities during 2025. Lenders across the region, on average, reported that about 20% of borrowers had an increase in carryover debt compared with last year. The average among all lenders was similar to last year and remained below the average from 2015-2020 in all states except Missouri.

Loan restructuring was slightly elevated as many borrowers adjusted to financial challenges, but loan denials remained minimal. The average share of loans that involved restructuring to meet liquidity needs was also similar to last year and below the average from 2016-2020 in all states except Missouri. The average share of loan requests that were denied because of cash flow or collateral shortages remained near 2% across the District but was also slightly higher in Missouri.

Despite ongoing challenges for crop producers, strong land valuations continued to support farm balance sheets and leverage among producers was steady. Across all respondents in the District, the average share of farm borrowers with a debt-to-asset ratio above 0.40 remained near 25%. About 50% of borrowers, on average, had more modest leverage with a ratio between 0.20 to 0.40 and the other 25% had low leverage.

A total of 129 lenders responded to the First Quarter Survey of Agricultural Credit Conditions in the Tenth Federal Reserve District — an area that includes Colorado, Kansas, Nebraska, Oklahoma, Wyoming, the northern half of New Mexico, and the western third of Missouri.

Oklahoma banker comments Q1 ’26

“Without extraordinary yields [in 2025] we would have significant carryover debt and restructuring requirements due to low commodity prices.”

“Livestock operators are profitable but capital requirements continue to escalate.”

“Lack of rain has wheat farmers struggling.”

Ty Kreitman is an associate economist in the Regional Affairs Department at the Omaha Branch of the Federal Reserve Bank of Kansas City.